DISCLAIMER - This is not investment advice and you should do your own due diligence. I make no representation, warranty or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information contained in this report. Any assumptions, opinions and estimates expressed in this report constitute my judgment as of the date thereof and is subject to change without notice. Any projections contained in the report are based on a number of assumptions, and there is no guarantee that projected outcomes will be achieved. I may, and likely do, have positions in the stocks I write about and may adjust or exit my positions without notice. I am not acting as your financial advisor or in any fiduciary capacity.

I’m following up my last report on Datadog with another high growth company and one that’s a bit more SMB focused, Monday.com. As before, I’ll spend a little less time on the product side to focus more on financial and operating metrics to make sense of the business.

Exec Summary

tldr; High growth company with a bad Q3 print that suggests trouble in the near-term that could put pressure on the stock even with the recent pullback. Pass or short based on valuation, and wait to see signs of new life.

Things I like

Growth has historically outpaced a very crowded field (Asana, Smartsheet, Freshworks) that suggests more market share capture and product strength

Integrations + automation workflows provide better footing to take on CRM, Freshworks, Jira, and other popular tools for new growth vectors

Elite 90% gross margins selling across SMB and enterprise (which is largely mid-market) shows relatively little discounting as they move upmarket

Strong FCF generation despite the heavy S&M spend; disciplined G&A and R&D investment

Things I don’t like / am monitoring

Q3 fell short across all customer segments, which could lead to tough times ahead, especially with the CRO change

Decreasing sales efficiency; up-market GTM has yet to ramp to more normal efficiencies while SMB trails other high growth benchmarks

AI functionality doesn’t seem to have driven uplift in new sales or upgrades

As an international company, quarterly earnings have less consistent disclosures, making it harder to call a comeback or future decline

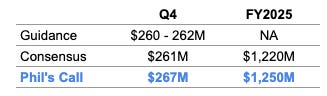

My Call on Q4 and FY25

With the noise in Q3, it’s hard to have strong conviction on my call here. I’d view Q4 revenue north of $269M as a great quarter, but anything short of $267M as further cause for concern the wheels are coming off.

Valuation

Stock trades at a 9.8x ‘25E revenue multiple today based on closing price of $248.90 on 1/24. While seemingly cheap compared to other high growth names, Monday has more volatility in its sales pipeline without obvious areas for easy growth to beat top and bottom-line expectations next year.

Conclusion: Pass / Short

The risk/reward ahead of Q4 is not all that attractive. I’d want to see a blowout Q4 quarter or macro indicator that international growth will re-accelerate to evaluate going long. I don’t have a great price target here because there’s too much uncertainty, but if I had to, I’d say $230-250 by year end.

In-depth Analysis

If you take a quick flip through the Monday investor deck, on the surface it seems like a pretty solid company. 30%+ revenue growth, operating leverage seen by FCF margins that have gone from close to breakeven to 28% in FY23 and 33% in Q3’24. To understand what’s going on now, it’s important to dissect revenue to see where growth is coming from and understand sales & marketing (the largest operating expense as % of revenue) to gauge future value.

A Closer Look at Revenue

By ARR & Customer Size

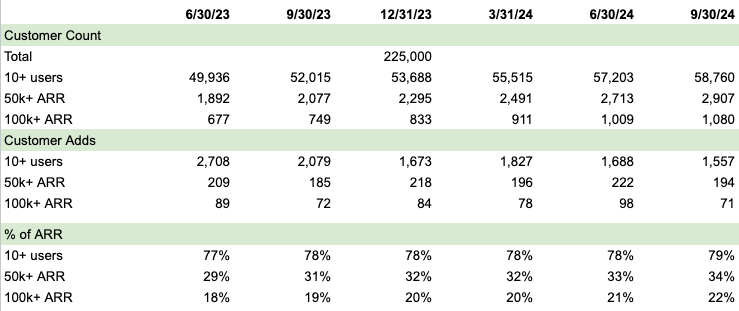

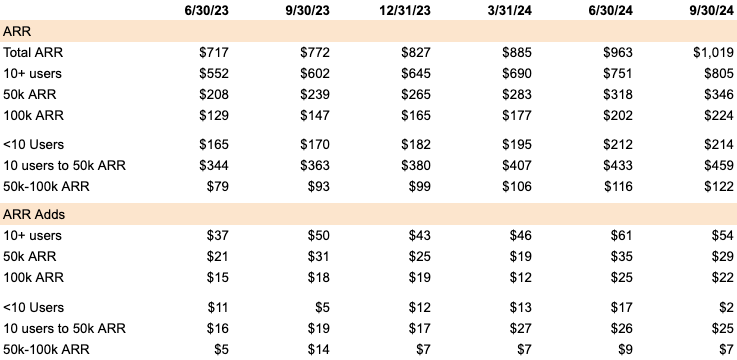

Although customer cohorts by ARR aren’t my favorite because customers can shift between different buckets and likely do, it’s what’s provided by management and useful for us to see what happened in Q3. The table below in green is what’s supplied by management, and the orange headers is my take based on ARR estimates. I’ve also imputed 3 customer segments (<10 users, 10 users - 50k ARR, and 50k-100k ARR) based on the disclosed figures.

When I look at Q3, a few things give me pause:

ARR add in the smallest segment. Monday only added $2M in ARR vs. $5M the year prior, and the lowest amount across the last 6 quarters. This is not where the sales focus is up-market, which is exactly what freaks me out. If the product-led growth segment is failing to generate or convert free trials, this to me says something about the broader demand environment that cannot be attributed to sales rep hiring or execution. You can chalk one quarter up to statistical variance, but for a chunk of the business that makes up 21% of ARR, growth needs to maintain on a certain glide path not to adversely impact the total top-line.

Upmarket also fared poorly. $100k+ ARR customers added $22M of ARR vs. $18M a year ago (24% growth), 50-100k ARR came in soft at $7M vs. $14M, which correlates with the customer adds comparing poorly to a year ago. Some of this can be attributed to sales execution and quarterly variance, but taken with low-end weakness, it suggests potential trouble across the full product suite.

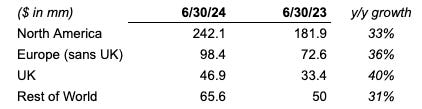

Geography

It gets harder to really break apart Monday’s business by geography, since we only get what they share periodically. The latest we have from their 1H’24 filing shows that Europe and the UK are growing faster than other regions. In November, investors got spooked when management spoke at the Nasdaq London investor conference. Here’s the relevant quote by the CFO and CEO responding to a question about demand environment:

So when we did Q3 results, we said that we saw some softness in the month of September and then October was better. We still see some choppiness in the market. Macro economy, still some challenges, mostly in Europe, Middle East and Asia Pacific. North America is stable. So broad-based, we are seeing some stability in some parts of the world, but still experiencing some challenges in other places. I can say that if you think about macro economy, it doesn't get any worse. I think actually, it gets better in some areas like North America, but still, we're not out of the...

Roy Mann

In EMEA, we see some softness.

Following that, the stock fell from a close of $290 to $276, and has continued to retreat further. To me, it’s interesting for management to disclose this: it’s incredibly easy to stick to a standard IR line of “we don’t comment on in quarter performance” and leave it at what they shared on the Q3 call1. For both the CFO and CEO to comment is telling, and sets up an opportunity on the Q4 call to say that the macro environment fell short. Whether that means a miss in terms of failing to handily beat guidance or even meet guidance is harder to say, but my read is that Q4 is likely to disappoint relative to prior years, with a small beat unlikely to impress.

One Other Q3 Data Point

In late August, Monday announced they crossed the $1B ARR mark. On its surface, the announcement feels like a nice achievement to tout without much impact. After all, the company did $236M in revenue in Q2, suggesting they were probably pretty close to $1B at the end of June anyway. So why do I care about this press release?

For a moment let’s assume that August 26 was the day they actually hit $1B ARR. Management saw it coming, wanted to give the company a pat on the back, drafted the press release, and then waited to cross the threshold before letting it hit the wire. That gives us a specific point in time where we know the company’s ARR. Can we use that to get smarter about how the quarter actually went?

If you read my other post on Datadog, you saw I applied a somewhat arbitrary multiplier of 1.03 to quarterly revenue to get to ARR. Let me share a bit more on how I think about ARR, especially for a more straightforward business like Monday’s2. A lot of the industry likes to take actual revenue in the quarter and equate that to ARR3. But that’s underestimating actual ARR. The only way actual revenue would equal ARR is if the company closed all new deals on Day 1 of the quarter, then sold nothing else, because subscription revenue is ratable, or recognized consistently across the time period. If you think about ARR sold in a quarter, the more back-end loaded those sales occurred (whether in Month 2 or Month 3 of the quarter), the less revenue you recognize, and the higher the multiplier should be. Additionally, more ARR sold in the quarter relative to the current ARR base also leads to a higher multiplier. As an investor, you rarely get enough information to perfectly decipher ARR, but you can get closer by applying a multiplier and triangulating with other KPIs and metrics shared by the company.

I estimate Q2’24 ending ARR at roughly $963M on 6/30/24, meaning Monday sold $37M worth of ARR in just under 2 months to get to the $1B mark. I would have estimated Q3 revenue to be roughly $249M without closing another deal at that point, with upside to $250M being driven by large enterprise deals closed in the final month. As we saw in the customer adds, 100k+ ARR customers came in far below what you’d expect for a high growth company, and revenue ended up at $251M.

What was the point of all this? Well, if there is a certain level of consistency and linearity in the business at the $50k ARR and below segments, I’d suspect there’s about $9-10M worth of in-quarter revenue contribution from new sales in those segments, and by the time management gives guidance by mid-Month 2 of the quarter, they have a high degree of confidence they’ll beat without any of the large deals that represent really overachievement. Turning to Q4, beating their revenue guidance of $260-262M doesn’t really tell me anything, as I’d expect they had good line of sight to do so when they reported. I’d also expect an aggressive sales push to close some enterprise deals and come in above that, which is why I’d set a baseline closer to $267M to measure Q4.

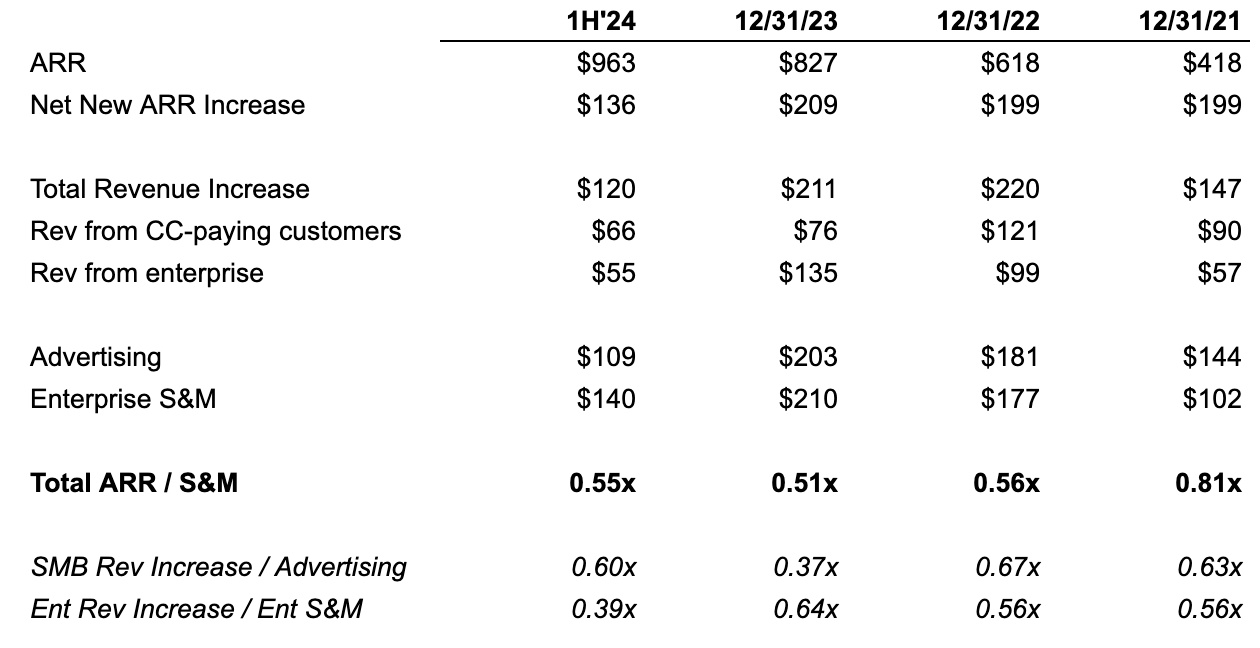

Making Sense of Sales Efficiency

You can think of Monday having two business lines - their SMB segment, and what they’ve called “enterprise” although I view more as upper mid-market. It’s worthwhile for us to get some more clarity on how effective GTM is for both segments, since it’ll let us benchmark them against other peers and forecast better how they’ll do in the future.

First, a definition and framework for how I’m approaching this. I’m going to categorize all advertising spending as product-led growth and SMB sales. This is admittedly unfair, as advertising is intended to raise awareness among enterprises as much as it is the SMBs who rely on this exposure, and there are likely other expenses I’m not capturing that are focused on PLG / SMB sales. Still, it’s the cleanest partition I’ve got. I’ll call the inverse, which is the remaining S&M spend enterprise S&M, which pertains more to the larger sales force that focuses time on contacting and selling to customers and prospects.

To get the numerator to understand sales efficiency, I’ve looked at the MD&A commentary and focused on “processing fees” within cost of sales. I’ve assumed these pertain directly to credit card sales and are roughly a 2.9% take, to figure out how much of the revenue increase in a period was due to customers paying by credit card, with the remainder coming from enterprises.

This isn’t perfect data, but it’s helpful to think about how the business is performing.

On an ARR basis, we see total efficiency trails others high growth names, which is unsurprising based on how much S&M spend there is. When we separate it into SMB and enterprise, we see SMB has run ahead of enterprise, although just slightly. 2023 had a bit of an aberration, with increase in processing fees dipping in what was likely a one-time outlier, and I also think on a revenue basis, 1H’24 likely misses some big ARR wins in Q2. However, we see that SMB remains a more efficient business than enterprise, but on its own, is not overly impressive with a payback period that takes over a year.

However, looking on a segmented basis, I see potential for better efficiency if they get the enterprise side of their house in-line with more of the broader sector and where I’d see operating leverage down the line.

Valuation

Monday has a market cap of $13.2B and enterprise value of $11.8B based on $248.90 closing price. The Street has them at FY2024 consensus revenue of $965M and $1.22B with 26% growth for 2025, implying 12.3x and 9.8x multiples. If the business doesn’t completely fall apart, 26% growth seems fairly reasonable with 11% built in just in a higher ending ARR, and 15% coming from modest upsells to their existing base and new customers. The issue I have stems more from what they’ll need to spend to get that growth, assuming most of it becomes enterprise driven. Investors that are spooked by management commentary for Q4 are unlikely to take well to much higher investment in sales, and any miss is likely to hammer the stock.

What Could Drive Upside?

With the current state of affairs, it’s tough to see near-term drivers for value to own it now. My sense is you’d have to believe growth will be better than expected and that the company can weather some of the near-term sales disruption that inserting a new global sales leader and adjustments to territories/comp plans/quotas can create.

On AI, I’m not convinced any of the OpenAI functionality they’ve added to the product suite has made much of a difference. Aside helping grow revenue more generally, I’d expect to see impact in 1) net retention rates, with Pro editions priced at 50-60% and AI adopters likely coming from existing customers, and 2) higher cost of sales / lower gross margins, with overall margin percentage coming down to reflect the higher compute associated with AI inference. Until I see either, there is probably more risk that AI more broadly is a disruptor that threatens to simplify some of the integrations and automation that make Monday so good.4

Separately, it’s early days for all the specialized products tackling CRM, ITSM, and dev project management. It could very well be that Monday’s workOS platform provides meaningful gains to win market share here, but these are markets with well capitalized and well known competitors, meaning it’s hard to see these sales as more efficient on an ARR basis relative to the core work management product.

Still, any company that can grow as quickly as Monday did and do so with strong gross margins shouldn’t be written off. There’s no reason not to keep tabs and start building a position once there’s confidence of enduring growth.

When you look at the ARR data and geographic data, a reasonable hypothesis is Q3 represents a baseline growth that’s primarily driven by North America, and that big beats like Monday saw in Q2 is driven more by EMEA. Until the annual filing gets released, we won’t be able to see whether this holds water. But if there is correlation, stock performance becomes a more straight-forward bet. Without strong EMEA results, you have a 20% grower that probably continues to trade at or below its current multiple. With a bounce back, I can see room to run but it’s hard to feel great about the probability of that today.

The answer provided by the CFO on the earnings call is as follows: Nevertheless, in Q3, we saw some continued choppiness in the macro, including pure enterprise customers, if you look at the total heads, which was impacted in part by slower hiring in sales. As I said, we had a very strong Q2, an outlier, and slower-than-expected growth in monday dev as we pivot to focus on developers. So I would say all of the above created some light September, but we're seeing already strong momentum in October.

Monday.com has a very simple rev rec policy, because it sells subscriptions in a straightforward manner: price per seat on a monthly or annual basis. You know the start and end date, and it’s a linear recognition of the total subscription amount.

Multiplied by 4. I’ll omit the implicit math back and forth to simplify.

I wrote almost all of this before the Deepseek news came out that has panicked investors about China’s AI advances, and the potential for cheaper, better models.